Key Takeaways:

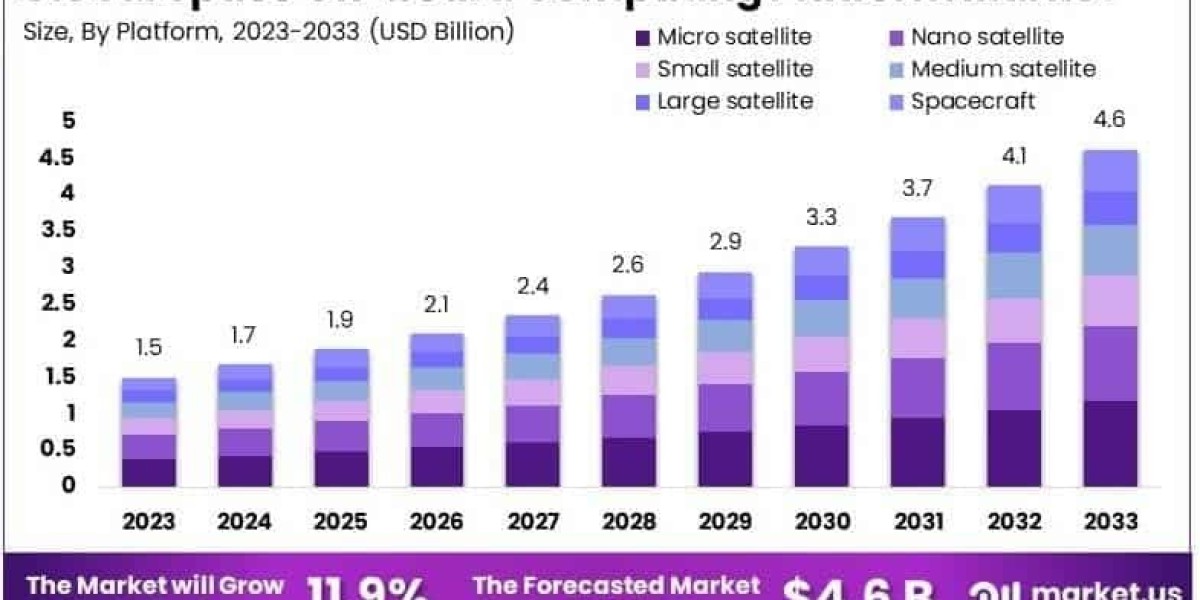

Market Size in 2023: USD 1.5 Billion

Estimated Market Size by 2033: USD 4.6 Billion

CAGR (2024–2033): 11.9%

Key Technology Driver: Edge AI integration and radiation-hardened processors

Growth Hotspots: LEO constellations and autonomous satellite networks

Dominant Market Position

North America currently dominates the space on-board computing platform market, backed by strong aerospace infrastructure, government space programs, and a mature private sector. Europe follows closely, propelled by pan-European space initiatives and increasing investments in defense and climate-monitoring satellites. The Asia-Pacific region is emerging as a high-growth frontier, driven by strategic investments in space exploration and national satellite programs. Dominant players are leveraging vertically integrated ecosystems and partnerships with launch providers and research institutions to solidify their foothold. Competitive advantage hinges on delivering ruggedized, fault-tolerant computing systems optimized for mission-critical and multi-orbit operations in diverse and extreme space environments.

Technology Perspective

Technologies fueling the space on-board computing platform market include radiation-hardened microprocessors, FPGAs, neuromorphic chips, and AI-enabled edge computing. Onboard platforms are increasingly adopting modular, software-defined architectures that allow real-time reconfiguration based on mission objectives. These systems are optimized for low power consumption, data throughput, and error resilience. Integration of machine learning enables spacecraft to process images, detect anomalies, and make autonomous decisions without ground control. Next-gen platforms also explore quantum-safe encryption, optical interconnects, and miniaturized AI accelerators. The shift from centralized to decentralized computing in orbit is defining the future of agile, intelligent, and responsive space missions across defense and commercial sectors.

Dynamic Landscape

The space on-board computing market is dynamic and innovation-driven, with new entrants challenging legacy players. Open hardware standards, reusable rockets, and global competition in satellite manufacturing intensify development. Strategic investments, government contracts, and startup accelerators are expanding the space-tech ecosystem at an unprecedented pace.

Drivers, Restraints, Opportunities, Challenges

Drivers: Satellite autonomy, data-driven missions, and AI edge processing.

Restraints: High R&D cost, limited launch cycles.

Opportunities: Deep space exploration, software-defined platforms.

Challenges: Radiation tolerance, thermal dissipation, system longevity.

Use Cases:

Real-time geospatial and Earth observation analytics

Autonomous spacecraft guidance and collision avoidance

On-orbit AI image processing and anomaly detection

Defense and tactical situational awareness

Deep space navigation and telemetry compression

Satellite-to-satellite communication and coordination

Key Players Analys

Market leaders are prioritizing innovation in on-board AI acceleration, fault-tolerant computing, and space-qualified chipsets. These firms leverage proprietary hardware-software stacks and often collaborate with space agencies and research bodies for mission alignment. The competitive edge lies in producing modular, scalable systems adaptable across LEO, MEO, and GEO missions. Advanced telemetry, mission reconfiguration capabilities, and edge analytics support are key differentiators. Players also focus on system miniaturization for CubeSats and compatibility with multiple payload architectures. By investing in cybersecurity, AI model optimization, and space-edge processing capabilities, they’re shaping the trajectory of autonomous space operations for both government and commercial sectors.

Recent Developments:

AI-integrated, radiation-hardened SoCs launched for satellite AI processing

Trials of reprogrammable FPGA-based systems for adaptive missions

Expansion of CubeSat-compatible computing modules

Partnerships formed to develop edge AI solutions for defense satellites

Open architecture initiatives to boost cross-platform satellite operability

Conclusion:

The Space On-board Computing Platform Market is at the forefront of enabling autonomous, responsive, and intelligent space operations. Fueled by technological breakthroughs and strategic space initiatives, the sector promises transformative capabilities in both commercial and defense segments. As demand for orbital data and autonomy grows, onboard computing becomes a vital pillar of the new space economy.